Beyond the Prize Draw: DigiGold vs Premium Bonds

By

![]() Checked by ,

Checked by ,

Updated

At the end of 2025, around 24 million people were believed to be holding Premium Bonds¹. In that context, The Royal Mint’s DigiGold products are still a relatively undiscovered opportunity, with just tens of thousands of investors currently holding Digital Gold, Digital Silver, Digital Platinum or Little Treasures.

Both Premium Bonds and DigiGold may appeal to long-term savers who want to set aside a fixed amount each month and gradually build a nest egg for retirement, a house deposit, or simply a rainy day fund. So how do they compare?

Premium Bonds

Premium Bonds are issued by National Savings & Investments (NS&I) on behalf of HM Treasury. They work a bit like a savings account, but rather than paying interest, bond holders are entered into a monthly prize draw.

Prizes range from £1 million down to £25 (or nothing at all!) and from April 2026 the odds of winning any prize in a given month will be around 23,000 to 1 for every £1 of bonds held². (For context, the chances of winning any prize in the National Lottery’s Lotto are 18.6 to 1 for every £1 spent – though you don’t get to retain your original stake with the Lotto!)

The money used to purchase Premium Bonds is effectively loaned to the UK Government and used to help fund public spending. Because the government has many different ways of borrowing money, the Premium Bond prize fund rate (the average return across all bond holders) tends to move broadly in line with wider interest rate trends.

We have seen this recently. From April 2026, the Premium Bond Prize Fund Rate will fall from 3.6% to 3.3%³.

This means that someone with average luck might expect their holdings to grow by roughly 3.3% per year over time. But because returns depend on the monthly prize draw, outcomes can vary widely. One person holding a single bond could win £1 million, while another person with a large holding could receive no prizes at all over the course of a year. In fact a recent Freedom of Information request revealed that 62% of bondholders have never won anything at all, though this is in part due to the lower values held by a large proportion of Premium Bond holders⁴.

DigiGold

DigiGold (previously Signature Gold) allows investors to buy small fractions of large 400oz gold bars stored in The Royal Mint’s purpose-built vault.

From just £25, investors can access the economies of scale associated with institutional-grade bullion. Purchases and sales can be made 24 hours a day based on live metal prices.

Importantly, DigiGold investors receive full legal title to the bullion they purchase. The Royal Mint acts solely as custodian, securely storing the metal in its vaults with no legal claim over the investor’s holdings.

The value of your investment can be tracked on the ‘Vaulted Investments’ section of your royalmint.com account and will fluctuate according to live metal prices – increasing when prices rise and declining if prices fall. Should you wish to sell your metal, you can do so at any time at the click of a button and The Royal Mint will buy the metal back from you according to prevailing international prices.

DigiGold is an investment in precious metal, and so unlike Premium Bonds, capital is at risk. Like with most investments, if metal prices fall you could see the value of your holdings drop below the value you invested, but if the metal prices rise you could see the value of your holdings exceed the amount originally invested, enabling you to sell and make a profit. Many DigiGold investors view the product as a long-term investment – something they hope will be worth more in the future even if short-term values can be volatile.

Premium Bonds and DigiGold Compared

| Premium Bonds | DigiGold (Digital Gold) | |

| How is my money used? | Loaned to the UK Government | Purchase of Physical Gold Bars in The Royal Mint's Vault |

| Source of Returns | Monthly Prize Draw | Gold Price Growth |

| Minimum Deposit/Investment | £25 | £25 |

| Maximum Total Amount | £50,000 | Unlimited |

| Buying / Selling Hours | 24/7 | 24/7 |

| Capital At Risk | No (Backed by UK Government) |

Yes (Falling gold price) |

| VAT | No | No |

| Capital Gains Tax | No | Yes (If profits exceed threshold in a tax year) |

| Ownership of Issuing Company | HM Treasury | HM Treasury |

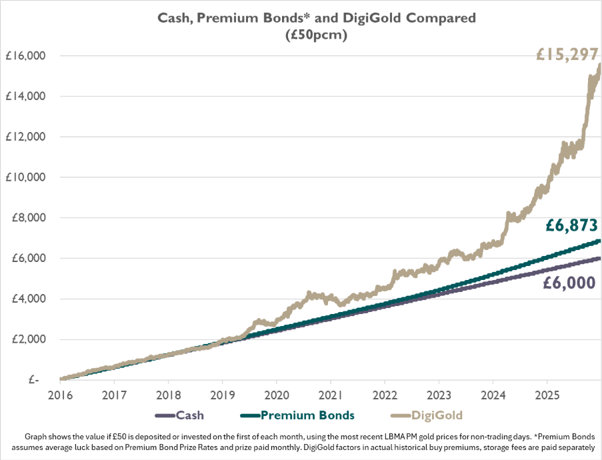

If you had saved or invested £50 per month over the past 10 years, the outcome would look very different depending on what you did with that money.

If you had simply placed £50 a month into a jar or under the mattress, you would now have £6,000; exactly what you put in.

Premium Bonds and DigiGold tell a different story.

Based on prize fund rates over the past 10 years and assuming average luck1, £50 invested each month into Premium Bonds over the same period would have grown to around £6,873.

Over that same 10-year period, however, £50 invested monthly into DigiGold would have reached approximately £15,297.

While DigiGold is not capital protected in the way Premium Bonds are, the comparison highlights how assets that can grow in value over time may deliver very different outcomes for long-term savers. The graph shows that over the past 10 years those willing to take the larger degree of risk would likely have significantly outperformed the more cautious option.

Of course, past performance does not guarantee future returns. The price of gold can rise and fall over shorter periods, and investors should always consider their own financial goals and tolerance for risk.

For long-term savers building wealth gradually each month, this distinction can matter. While Premium Bonds offer certainty of capital, the expected return is linked to government borrowing conditions. Gold, by contrast, reflects global demand for a scarce asset that cannot be created by central banks or governments.

This is why many investors choose not to view the two as direct competitors, but as complementary tools. Premium Bonds can provide stability and the chance of a prize, while DigiGold offers a simple way to build a position in physical gold over time.

For those looking beyond the prize draw and considering how best to build long-term savings, even small monthly allocations to gold can make a meaningful difference over time.

Notes

The content of this article is accurate at the time of publishing, is for general information purposes only, and does not constitute investment, legal, tax or any other advice. Before making any investment or financial decision, you may wish to seek advice from your financial, legal, tax and/or accounting advisers. This article may include references to third-party sources. We do not endorse or guarantee the accuracy of information from external sources, and readers should verify all information independently and use external sources at their own discretion. We are not responsible for any content or consequences arising from such third-party sources.